Evaluates the convexity for a security.

Synopsis

#include <imsl.h>

float

imsl_f_convexity (struct

tm settlement, struct

tm maturity,

float coupon_rate, float yield, int frequency, int basis)

The type double function is imsl_d_convexity.

Required Arguments

struct tm

settlement (Input)

The date on which payment is made to

settle a trade. For a more detailed discussion on dates see the Usage Notes section of

this chapter.

struct tm maturity

(Input)

The date on which the bond comes due, and principal and accrued

interest are paid. For a more detailed discussion on dates see the Usage Notes section of

this chapter.

float

coupon_rate (Input)

Annual interest rate set forth on the

face of the security; the coupon rate.

float yield

(Input)

Annual yield of the security.

int frequency

(Input)

Frequency of the interest payments. It should be one of

IMSL_ANNUAL,

IMSL_SEMIANNUAL

or IMSL_QUARTERLY. For a

more detailed discussion on frequency see the

Usage Notes

section of this chapter.

int basis

(Input)

The method for computing the number of days between two dates. It

should be one of IMSL_DAY_CNT_BASIS_ACTUALACTUAL,

IMSL_DAY_CNT_BASIS_NASD,

IMSL_DAY_CNT_BASIS_ACTUAL360,

IMSL_DAY_CNT_BASIS_ACTUAL365,

or IMSL_DAY_CNT_BASIS_30E360.

. For a more detailed discussion see the Usage Notes section of this

chapter.

Return Value

The convexity for a security. If no result can be computed, NaN is returned.

Description

Function imsl_f_convexity computes the convexity for a security. Convexity is the sensitivity of the duration of a security to changes in yield.

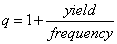

It is computed using the following:

where n is calculated from imsl_coupon_number,

and  .

.

Example

In this example, imsl_f_convexity computes the convexity for a security with the settlement date of July 1, 1990, and maturity date of July 1, 2000, using the Actual/365 day count method.

#include <stdio.h>

#include "imsl.h"

void main()

{

struct tm settlement, maturity;

float coupon = .075;

float yield = .09;

int frequency = IMSL_SEMIANNUAL;

int basis = IMSL_DAY_CNT_BASIS_ACTUAL365;

float convexity;

settlement.tm_year = 90;

settlement.tm_mon = 6;

settlement.tm_mday = 1;

maturity.tm_year = 100;

maturity.tm_mon = 6;

maturity.tm_mday = 1;

convexity = imsl_f_convexity (settlement, maturity,

coupon, yield, frequency, basis);

printf ("The convexity of the bond with ");

printf ("semiannual interest payments is %.4f.\n", convexity);

}

Output

The convexity of the bond with semiannual interest payments is 59.4050.

|

Visual Numerics, Inc. PHONE: 713.784.3131 FAX:713.781.9260 |