Computes estimates of the parameters of a GARCH(p,q) model.

Synopsis

#include <imsls.h>

float *imsls_f_garch (int p, int q, int m, float y[], float xguess[], …, 0)

The type double function is imsls_d_garch.

Required Arguments

int p

(Input)

Number of GARCH parameters.

int q

(Input)

Number of ARCH parameters.

int m

(Input)

Length of the observed time series.

float y[]

(Input)

Array of length m containing the

observed time series data.

float xguess[]

(Input)

Array of length p + q + 1 containing the initial values for the parameter array x[].

Return Value

Pointer to the parameter array x[] of length p + q + 1 containing the estimated values of sigma squared, followed by the q ARCH parameters, and the p GARCH parameters.

Synopsis with Optional Arguments

#include <imsls.h>

float *imsls_f_garch (int p, int q, int m, float y[], float xguess[], IMSLS_MAX_SIGMA, float max_sigma,

IMSLS_A, float *a,

IMSLS_AIC, float *aic,

IMSLS_VAR, float *var,

IMSLS_VAR_USER, float var[],

IMSLS_VAR_COL_DIM, int var_col_dim,

IMSLS_RETURN_USER, float x[],

0)

Optional Arguments

IMSLS_MAX_SIGMA,

float max_sigma, (Input)

Value of the upperbound on the

first element (sigma) of the array of returned estimated coefficients.

Default = 10.

IMSLS_A,

float *a, (Output)

Value of Log-likelihood function

evaluated at the estimated parameter array x.

IMSLS_AIC,

float *aic, (Output)

Value of Akaike Information Criterion

evaluated at the estimated parameter array x.

IMSLS_VAR,

float *var, (Output)

Array of size

(p+q+1)x(p+q+1) containing the variance-covariance

matrix.

IMSLS_VAR_USER,

float var[], (Output)

Storage for array var is provided by

the user.

See IMSLS_VAR.

IMSLS_VAR_COL_DIM,

int var_col_dim, (Input)

Column dimension (p+q+1)of the

variance-covariance matrix.

IMSLS_RETURN_USER,

float x[], (Output)

If specified, x returns an array of

length p +q + 1 containing the estimated values of sigma

squared, followed by the q ARCH parameters, and the p GARCH

parameters. Storage for estimated parameter array x is provided by the

user.

Description

The Generalized Autoregressive Conditional Heteroskedastic

(GARCH) model for a time series  is defined as

is defined as

where zt’s are independent and identically distributed standard normal random variables,

The above model is denoted as GARCH(p,q). The βi and αi coeffecients will be referred to as GARCH and ARCH coefficents, respectively. When βi = 0, i = 1,2,…,p, the above model reduces to ARCH(q) which was proposed by Engle (1982). The nonnegativity conditions on the parameters imply a nonnegative variance and the condition on the sum of the βi’s and α i’s is required for wide sense stationarity.

In the empirical analysis of observed data, GARCH(1,1) or GARCH(1,2) models have often found to appropriately account for conditional heteroskedasticity (Palm 1996). This finding is similar to linear time series analysis based on ARMA models.

It is important to notice that for the above models positive and negative past values have a symmetric impact on the conditional variance. In practice, many series may have strong asymmetric influence on the conditional variance. To take into account this phenomena, Nelson (1991) put forward Exponential GARCH (EGARCH). Lai (1998) proposed and studied some properties of a general class of models that extended linear relationship of the conditional variance in ARCH and GARCH into nonlinear fashion.

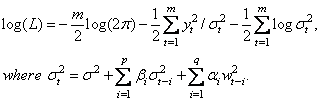

The maximum likelihood method is used in estimating the parameters in GARCH(p,q). The log-likelihood of the model for the observed series {wt} with length m = nobs is

Thus log(L) is maximized subject to the constraints on the αi, βi, and s.

In this model, if q = 0, the GARCH model is singular since the estimated Hessian matrix is singular.

The initial values of the parameter vector x entered in vector xguess must satisfy certain constraints. The first element of xguess refers to s2 and must be greater than zero and less than max_sigma. The remaining p+q initial values must each be greater than or equal to zero and sum to a value less than one.

To guarantee stationarity in model fitting,

is checked internally. The initial values should selected from values between zero and one.

AIC is computed by

- 2 log (L) + 2(p+q+1),

where log(L) is the value of the log-likelihood function.

Statistical inferences can be performed outside the routine GARCH based on the output of the log-likelihood function (A), the Akaike Information Criterion (AIC), and the variance-covariance matrix (VAR).

Example

The data for this example are generated to follow a GARCH(p,q) process by using a random number generation function sgarch. The data set is analyzed and estimates of sigma, the ARCH parameters, and the GARCH parameters are returned. The values of the Log-likelihood function and the Akaike Information Criterion are returned from the optional arguments IMSLS_A and IMSLS_AIC.

#include <imsls.h>

#include <math.h>

static void sgarch (int p, int q, int m, float x[],

float y[], float z[], float y0[], float sigma[]);

#define M 1000

#define N (P + Q + 1)

#define P 2

#define Q 1

void main ()

{

int n, p, q, m;

float a, aic, wk1[M + 1000], wk2[M + 1000],

wk3[M + 1000], x[N], xguess[N], y[M];

float *result;

imsls_random_seed_set (182198625);

m = M;

p = P;

q = Q;

n = p+q+1;

x[0] = 1.3;

x[1] = .2;

x[2] = .3;

x[3] = .4;

xguess[0] = 1.0;

xguess[1] = .1;

xguess[2] = .2;

xguess[3] = .3;

sgarch (p, q, m, x, y, wk1, wk2, wk3);

result = imsls_f_garch(p, q, m, y, xguess,

IMSLS_A, &a,

IMSLS_AIC, &aic,

0);

printf("Sigma estimate is\t%11.4f\n", result[0]);

printf("ARCH(1) estimate is\t%11.4f\n", result[1]);

printf("GARCH(1) estimate is\t%11.4f\n", result[2]);

printf("GARCH(2) estimate is\t%11.4f\n", result[3]);

printf("\nLog-likelihood function value is\t%11.4f\n", a);

printf("Akaike Information Criterion value is\t%11.4f\n", aic);

return;

}

static void sgarch (int p, int q, int m, float x[],

float y[], float z[], float y0[], float sigma[])

{

int i, j, l;

float s1, s2, s3;

imsls_f_random_normal ( m + 1000, IMSLS_RETURN_USER, z, 0);

l = imsls_i_max (p, q);

l = imsls_i_max (l, 1);

for (i = 0; i < l; i++) y0[i] = z[i] * x[0];

/* COMPUTE THE INITIAL VALUE OF SIGMA */

s3 = 0.0;

if (imsls_i_max (p, q) >= 1) {

for (i = 1; i < (p + q + 1); i++) s3 += x[i];

}

for (i = 0; i < l; i++) sigma[i] = x[0] / (1.0 - s3);

for (i = l; i < (m + 1000); i++) {

s1 = 0.0;

s2 = 0.0;

if (q >= 1) {

for (j = 0; j < q; j++)

s1 += x[j + 1] * y0[i - j - 1] * y0[i - j - 1];

}

if (p >= 1) {

for (j = 0; j < p; j++)

s2 += x[q + 1 + j] * sigma[i - j - 1];

}

sigma[i] = x[0] + s1 + s2;

y0[i] = z[i] * sqrt (sigma[i]);

}

/*

* DISCARD THE FIRST 1000 SIMULATED OBSERVATIONS

*/

for (i = 0; i < m; i++) y[i] = y0[1000 + i];

return;

} /* end of function */

Output

Sigma estimate is 1.6480

ARCH(1) estimate is 0.2427

GARCH(1) estimate is 0.3175

GARCH(2) estimate is 0.3335

Log-likelihood function value is -2707.0903

Akaike Information Criterion value is 5422.1807

|

Visual Numerics, Inc. PHONE: 713.784.3131 FAX:713.781.9260 |