.p>.CSCH12.DOC!RANDOM_ARMA;random_arma

Generates a time series from a specific ARMA model.

Synopsis

#include <imsls.h>

float *imsls_f_random_arma (int n_observations, int p, float ar[], int q, float ma[], ..., 0)

The type double function is imsls_d_random_arma.

Required Arguments

int

n_observations (Input)

Number

of observations to be generated. Parameter n_observations must be greater than or equal to one.

int

p (Input)

Number of

autoregressive parameters. Paramater p must be greater than or equal to zero.

float

ar[] (Input)

Array of length

p containing the autoregressive parameters.

int

q (Input)

Number of moving

average parameters. Parameter q must be greater than or equal to zero.

float

ma[] (Input)

Array of length

q containing the moving average parameters.

Return Value

An array of length n_observations containing the generated time series.

Synopsis with Optional Arguments

#include <imsls.h>

float

*imsls_f_random_arma (int

n_observations, int p, float

ar[],

int q, float ma[],

IMSLS_ARMA_CONSTANT, float

constant,

IMSLS_VAR_NOISE, float

*a_variance,

IMSLS_INPUT_NOISE, float

*a_input,

IMSLS_OUTPUT_NOISE, float

**a_return,

IMSLS_OUTPUT_NOISE_USER, float

a_return[],

IMSLS_NONZERO_ARLAGS, int

*ar_lags,

IMSLS_NONZERO_MALAGS, int

*ma_lags,

IMSLS_INITIAL_W, float

*w_initial,

IMSLS_ACCEPT_REJECT_METHOD,

IMSLS_RETURN_USER, float w[],

0)

Optional Arguments

IMSLS_ARMA_CONSTANT, float constant

(Input)

Overall constant. See “Description”.

Default: constant =

0

IMSLS_VAR_NOISE, float

a_variance (Input)

If IMSLS_VAR_NOISE is

specified (and IMSLS_INPUT_NOISE is

not specified) the noise at will be generated from a normal

distribution with mean 0 and variance a_variance.

Default:

a_variance =

1.0

IMSLS_INPUT_NOISE, float *a_input

(Input)

If IMSLS_INPUT_NOISE is

specified, the user will provide an array of length n_observations +

max (ma_lags[i])

containing the random noises. If this option is specified, then IMSLS_VAR_NOISE should

not be specified (a warning message will be issued and the option IMSLS_VAR_NOISE will

be ignored).

IMSLS_OUTPUT_NOISE, float

**a_return (Output)

An address of a pointer to an

internally allocated array of length n_observations + max

(ma_lags[i])

containing the random noises.

IMSLS_OUTPUT_NOISE_USER, float

a_return[] (Output)

Storage for array a_return is provided

by user. See IMSLS_OUTPUT_NOISE.

IMSLS_NONZERO_ARLAGS, int ar_lags[]

(Input)

An array of length p containing the order

of the nonzero autoregressive parameters.

Default: ar_lags = [1,

2, ..., p]

IMSLS_NONZERO_MALAGS, int ma_lags

(Input)

An array of length q containing the order

of the nonzero moving average parameters.

Default: ma_lags = [1, 2, ...,

q]

IMSLS_INITIAL_W, float

w_initial[] (Input)

Array of length max (ar_lags[i])

containing the initial values of the time series.

Default: all the elements

in w_initial =

constant/(1 − ar [0] − ar [1] − … − ar [p − 1])

IMSLS_ACCEPT_REJECT_METHOD

(Input)

If IMSLS_ACCEPT_REJECT_METHOD

is specified, the random noises will be generated from a normal distribution

using an acceptance/rejection method. If IMSLS_ACCEPT_REJECT_METHOD

is not specified, the random noises will be generated using an inverse

normal CDF method. This argument will be ignored if IMSLS_INPUT_NOISE is

specified.

IMSLS_RETURN_USER, float r[]

(Output)

User-supplied array of length n_random containing

the generated time series.

Description

Function imsls_f_random_arma

simulates an ARMA(p, q) process, {Wt}, for

t =

1, 2, ..., n (with n = n_observations,

p = p,

and q = q).

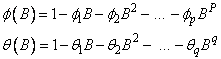

The model is

Let μ be the mean of the time series {Wt}. The overall constant θ0 (constant) is

Time series whose innovations have a nonnormal distribution may be simulated by providing the appropriate innovations in a_input and start values in w_initial.

The time series is generated according to the followng model:

X[i] = constant + ar[0] ∙ X[i − ar_lags[0] ] + … +

ar[p − 1] ∙ X[i − ar_lags[p − 1] ] +

A[i] − ma[0] ∙ A[i − ma_lags[0] ] − … −

ma[q − 1] ∙ A[i − ma_lags[q − 1] ]

where the constant is related to the mean of the series,

as follows:

and where

X[t] = W[t], t = 0, 1, …, n_observations − 1

and

W[t] = w_initial[t + p], t = −p, −p + 1, …, −2, −1

and A is either a_input (if IMSLS_INPUT_NOISE is specified) or a_return (otherwise).

Examples

Example 1

In this example, imsls_f_random_arma is used to generate a time series of length five, using an ARMA model with three autoregressive parameters and two moving average parameters. The start values are 0.1000, 0.0500, and 0.0375.

#include <stdio.h>

#include <imsls.h>

void main()

{

int n_random = 5;

int np = 3;

float phi[3] = {0.5, 0.25, 0.125};

int nq = 2;

float theta[2] = {-0.5, -0.25};

float *r;

imsls_random_seed_set(123457);

r = imsls_f_random_arma(n_random, np, phi, nq, theta, 0);

imsls_f_write_matrix("ARMA random deviates:",

1, n_random, r, IMSLS_NO_COL_LABELS, 0);

}

Output

ARMA random deviates:

0.863 0.809 1.904 0.110 2.266

Example 2

In this example, a time series of length 5 is generated using an ARMA model with 4 autoregressive parameters and 2 moving average parameters. The start values are 0.1, 0.05 and 0.0375.

#include <stdio.h>

#include <imsls.h>

void main()

{

int n_random = 5;

int np = 3;

float phi[3] = {0.5, 0.25, 0.125};

int nq = 2;

float theta[2] = {-0.5, -0.25};

float wi[3] = {0.1, 0.05, 0.0375};

float theta0 = 1.0;

float avar = 0.1;

float *r;

imsls_random_seed_set(123457);

r = imsls_f_random_arma(n_random, np, phi, nq, theta,

IMSLS_ACCEPT_REJECT_METHOD,

IMSLS_INITIAL_W, wi,

IMSLS_ARMA_CONSTANT, theta0,

IMSLS_VAR_NOISE, avar,

0);

imsls_f_write_matrix("ARMA random deviates:",

1, n_random, r, IMSLS_NO_COL_LABELS, 0);

}

Output

ARMA random deviates:

1.403 2.220 2.286 2.888 2.832

Warning Errors

IMSLS_RNARM_NEG_VAR VAR(a) = “a_variance” = #, VAR(a) must be greater than 0. The absolute value of # is used for VAR(a).

IMSLS_RNARM_IO_NOISE Both IMSLS_INPUT_NOISE and IMSLS_OUTPUT_NOISE are specified. IMSLS_INPUT_NOISE is used.

|

Visual Numerics, Inc. PHONE: 713.784.3131 FAX:713.781.9260 |