Evaluates the effective annual interest rate.

Synopsis

#include <imsl.h>

float imsl_f_effective_rate (float nominal_rate, int n_periods)

The type double function is imsl_d_effective_rate.

Required Arguments

float nominal_rate

(Input)

The interest rate as stated on the face of a security.

int n_periods

(Input)

Number of compounding periods per year.

Return Value

The effective annual interest rate. If no result can be computed, NaN is returned.

Description

Function imsl_f_effective_rate computes the continuously-compounded interest rate equivalent to a given periodically-compounded interest rate. The nominal interest rate is the periodically-compounded interest rate as stated on the face of a security.

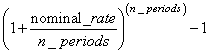

It can found by solving the following:

Example

In this example, imsl_f_effective_rate computes the effective annual interest rate of the nominal interest rate, 6%, compounded quarterly.

#include <stdio.h>

#include <imsl.h>

int main()

{

float nominal_rate = .06;

int n_periods = 4;

float effective_rate;

effective_rate = imsl_f_effective_rate (nominal_rate, n_periods);

printf ("The effective rate of the nominal rate, 6.0%%, ");

printf ("compounded quarterly is %.2f%%.\n", effective_rate * 100.);

}

Output

The effective rate of the nominal rate, 6.0%, compounded quarterly is 6.14%.