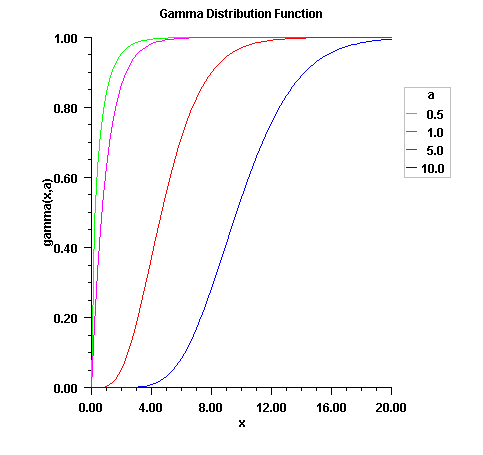

Evaluates the gamma cumulative probability distribution function.

Parameters

- x

- A

doublespecifying the argument at which the function is to be evaluated. - a

- A

doublespecifying the shape parameter. This must be positive.

Return Value

A double specifying the probability that a gamma random variable takes on a value less than or equal to x.

Remarks

Method Gamma evaluates the distribution function, F, of a gamma random variable with shape parameter a; that is,

where ![]() is the gamma function. (The gamma function is the integral from 0 to

is the gamma function. (The gamma function is the integral from 0 to ![]() of the same integrand as above). The value of the distribution function at the point x is the probability that the random variable takes a value less than or equal to x.

of the same integrand as above). The value of the distribution function at the point x is the probability that the random variable takes a value less than or equal to x.

The gamma distribution is often defined as a two-parameter distribution with a scale parameter b (which must be positive), or even as a three-parameter distribution in which the third parameter c is a location parameter. In the most general case, the probability density function over ![]() is

is

If T is such a random variable with parameters a, b, and c, the probability that ![]() can be obtained from

can be obtained from Gamma by setting ![]() .

.

If X is less than a or if X is less than or equal to 1.0, Gamma uses a series expansion. Otherwise, a continued fraction expansion is used. (See Abramowitz and Stegun, 1964.)

See Also

Cdf Class | Imsl.Stat Namespace | Example