Returns the effective annual interest rate.

Namespace:

Imsl.Finance

Assembly:

ImslCS (in ImslCS.dll) Version: 6.5.0.0

Syntax

Syntax

| C# |

|---|

public static double Effect( double nominalRate, int nper ) |

| Visual Basic (Declaration) |

|---|

Public Shared Function Effect ( _ nominalRate As Double, _ nper As Integer _ ) As Double |

| Visual C++ |

|---|

public: static double Effect( double nominalRate, int nper ) |

Parameters

- nominalRate

- Type: System..::.Double

A double which specifies the nominal interest rate.

- nper

- Type: System..::.Int32

A int which specifies the number of compounding periods per year.

Return Value

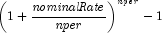

A double which specifies the effective annual interest rate.Remarks

The nominal interest rate is the periodically-compounded interest

rate as stated on the face of a security. The effective annual

interest rate is computed using the following: