Returns the internal rate of return for a schedule of cash flows.

Namespace:

Imsl.Finance

Assembly:

ImslCS (in ImslCS.dll) Version: 6.5.0.0

Syntax

Syntax

| C# |

|---|

public static double Xirr( double[] pmt, DateTime[] dates ) |

| Visual Basic (Declaration) |

|---|

Public Shared Function Xirr ( _ pmt As Double(), _ dates As DateTime() _ ) As Double |

| Visual C++ |

|---|

public: static double Xirr( array<double>^ pmt, array<DateTime>^ dates ) |

Parameters

- pmt

- Type: array<

System..::.Double

>[]()[]

A double array which contains cash flow values which correspond to a schedule of payments in dates.

- dates

- Type: array<

System..::.DateTime

>[]()[]

A DateTime array which contains a schedule of payment dates.

Return Value

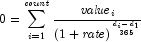

A double which specifies the internal rate of return.Remarks

It is not necessary that the cash flows be periodic. It can be found

by solving the following:

In the equation above, ![]() represents the

represents the

![]() th payment date.

th payment date. ![]() represents the 1st payment date.

represents the 1st payment date. ![]() represents the

represents the ![]() th cash flow.

th cash flow.

![]() is the internal rate of return.

is the internal rate of return.