com.imsl.stat.ARMA

com.imsl.stat.ARMA

|

JMSLTM Numerical Library 6.0 | |||||||

| PREV CLASS NEXT CLASS | FRAMES NO FRAMES | |||||||

| SUMMARY: NESTED | FIELD | CONSTR | METHOD | DETAIL: FIELD | CONSTR | METHOD | |||||||

java.lang.Object

public class ARMA

Computes least-square estimates of parameters for an ARMA model.

Class ARMA computes estimates of parameters for a

nonseasonal ARMA model given a sample of observations,

![]() , for

, for ![]() ,

where n =

,

where n = z.length.

Two methods of parameter estimation, method of moments and least squares,

are provided. The user can choose a method using the setMethod

method. If the user wishes to use the least-squares algorithm, the

preliminary estimates are the method of moments estimates by default.

Otherwise, the user can input initial estimates by using the

setInitialEstimates method. The following table lists the appropriate

methods for both the method of moments and least-squares algorithm:

| Least Squares | Both Method of Moment and Least Squares |

setCenter |

|

setARLags |

setMethod |

setMALags |

setRelativeError |

setBackcasting |

setMaxIterations |

setConvergenceTolerance |

setMean |

setInitialEstimates |

getMean |

getResidual |

getAutocovariance |

getSSResidual |

getVariance |

getParamEstimatesCovariance |

getConstant |

getAR |

|

getMA |

Method of Moments Estimation

Suppose the time series ![]() is generated by an

ARMA (p, q) model of the form

is generated by an

ARMA (p, q) model of the form

![]()

![]()

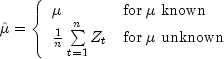

Let ![]() be the estimate of the

mean

be the estimate of the

mean ![]() of the time series

of the time series ![]() ,

where

,

where ![]() equals the following:

equals the following:

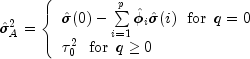

The autocovariance function is estimated by

![]()

for ![]() , where

K = p + q. Note that

, where

K = p + q. Note that ![]() is an estimate of the sample variance.

is an estimate of the sample variance.

Given the sample autocovariances, the function computes the method of moments estimates of the autoregressive parameters using the extended Yule-Walker equations as follows:

![]()

where

![]()

![]()

![]()

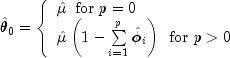

The overall constant ![]() is estimated by

the following:

is estimated by

the following:

The moving average parameters are estimated based on a system of

nonlinear equations given K = p + q + 1 autocovariances,

![]() , and

p autoregressive parameters

, and

p autoregressive parameters ![]() for

for

![]() .

.

Let ![]() . The autocovariances of the

derived moving average process

. The autocovariances of the

derived moving average process ![]() are

estimated by the following relation:

are

estimated by the following relation:

The iterative procedure for determining the moving average parameters is based on the relation

![]()

where ![]() denotes the autocovariance

function of the original

denotes the autocovariance

function of the original ![]() process.

process.

Let ![]() and

and

![]() , where

, where

![]()

and

![]()

Then, the value of ![]() at the (i + 1)-th iteration

is determined by the following:

at the (i + 1)-th iteration

is determined by the following:

![]()

The estimation procedure begins with the initial value

![]()

and terminates at iteration i when either ![]() is less than

is less than relativeError or i

equals iterations. The moving average parameter estimates are

obtained from the final estimate of ![]() by setting

by setting

![]()

The random shock variance is estimated by the following:

See Box and Jenkins (1976, pp. 498-500) for a description of a function that performs similar computations.

Least-squares Estimation

Suppose the time series ![]() is generated by a

nonseasonal ARMA model of the form,

is generated by a

nonseasonal ARMA model of the form,

![]()

where B is the backward shift operator, ![]() is the mean of

is the mean of ![]() , and

, and

![]()

![]()

with p autoregressive and q moving average parameters. Without loss of generality, the following is assumed:

![]()

![]()

so that the nonseasonal ARMA model is of order

![]() , where

, where ![]() and

and ![]() . Note that the usual hierarchical

model assumes the following:

. Note that the usual hierarchical

model assumes the following:

![]()

![]()

Consider the sum-of-squares function

![]()

where

![]()

and T is the backward origin. The random shocks

![]() are assumed to be independent and identically

distributed

are assumed to be independent and identically

distributed

![]()

random variables. Hence, the log-likelihood function is given by

![]()

where ![]() is a function of

is a function of

![]() .

.

For T = 0, the log-likelihood function is

conditional on the past values of both ![]() and

and

![]() required to initialize the model. The method of

selecting these initial values usually introduces transient bias into the

model (Box and Jenkins 1976, pp. 210-211). For

required to initialize the model. The method of

selecting these initial values usually introduces transient bias into the

model (Box and Jenkins 1976, pp. 210-211). For ![]() ,

this dependency vanishes, and estimation problem concerns maximization of

the unconditional log-likelihood function. Box and Jenkins (1976, p. 213)

argue that

,

this dependency vanishes, and estimation problem concerns maximization of

the unconditional log-likelihood function. Box and Jenkins (1976, p. 213)

argue that

![]()

dominates

![]()

The parameter estimates that minimize the sum-of-squares function are called least-squares estimates. For large n, the unconditional least-squares estimates are approximately equal to the maximum likelihood-estimates.

In practice, a finite value of T will enable sufficient

approximation of the unconditional sum-of-squares function. The values of

![]() needed to compute the unconditional sum of

squares are computed iteratively with initial values of

needed to compute the unconditional sum of

squares are computed iteratively with initial values of ![]() obtained by back forecasting. The residuals (including backcasts), estimate

of random shock variance, and covariance matrix of the final parameter

estimates also are computed. ARIMA parameters can be computed by using

obtained by back forecasting. The residuals (including backcasts), estimate

of random shock variance, and covariance matrix of the final parameter

estimates also are computed. ARIMA parameters can be computed by using

Difference with ARMA.

Forecasting

The Box-Jenkins forecasts and their associated probability limits for a

nonseasonal ARMA model are computed given a sample of

n = z.length, ![]() for

for ![]() .

.

Suppose the time series ![]() is generated by a

nonseasonal ARMA model of the form

is generated by a

nonseasonal ARMA model of the form

![]()

for ![]() ,

where B is the backward shift operator,

,

where B is the backward shift operator, ![]() is the constant, and

is the constant, and

![]()

![]()

with p autoregressive and q moving average parameters. Without loss of generality, the following is assumed:

![]()

![]()

so that the nonseasonal ARMA model is of order

![]() , where

, where ![]() and

and ![]() . Note that the usual hierarchical

model assumes the following:

. Note that the usual hierarchical

model assumes the following:

![]()

![]()

The Box-Jenkins forecast at origin t for lead time l of

![]() is defined in terms of the difference equation

is defined in terms of the difference equation

![]()

![]()

where the following is true:

![]()

![]()

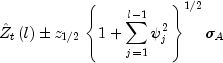

The ![]() percent probability limits for

percent probability limits for

![]() are given by

are given by

where ![]() is the

is the

![]() percentile of the standard normal

distribution

percentile of the standard normal

distribution

![]()

and

![]()

are the parameters of the random shock form of the difference equation.

Note that the forecasts are computed for lead times

![]() at origins

at origins

![]() , where

, where

![]() and

and

![]() .

.

The Box-Jenkins forecasts minimize the mean-square error

![]()

Also, the forecasts can be easily updated according to the following equation:

![]()

This approach and others are discussed in Chapter 5 of Box and Jenkins (1976).

| Nested Class Summary | |

|---|---|

static class |

ARMA.IllConditionedException

The problem is ill-conditioned. |

static class |

ARMA.IncreaseErrRelException

The bound for the relative error is too small. |

static class |

ARMA.MatrixSingularException

The input matrix is singular. |

static class |

ARMA.NewInitialGuessException

The iteration has not made good progress. |

static class |

ARMA.TooManyCallsException

The number of calls to the function has exceeded the maximum number of iterations times the number of moving average (MA) parameters + 1. |

static class |

ARMA.TooManyFcnEvalException

Maximum number of function evaluations exceeded. |

static class |

ARMA.TooManyITNException

Maximum number of iterations exceeded. |

static class |

ARMA.TooManyJacobianEvalException

Maximum number of Jacobian evaluations exceeded. |

| Field Summary | |

|---|---|

static int |

LEAST_SQUARES

Indicates autoregressive and moving average parameters are estimated by a least-squares procedure. |

static int |

METHOD_OF_MOMENTS

Indicates autoregressive and moving average parameters are estimated by a method of moments procedure. |

| Constructor Summary | |

|---|---|

ARMA(int p,

int q,

double[] z)

Constructor for ARMA. |

|

| Method Summary | |

|---|---|

void |

compute()

Computes least-square estimates of parameters for an ARMA model. |

double[][] |

forecast(int nForecast)

Computes forecasts and their associated probability limits for an ARMA model. |

double[] |

getAR()

Returns the final autoregressive parameter estimates. |

double[] |

getAutoCovariance()

Returns the autocovariances of the time series z. |

int |

getBackwardOrigin()

Returns the user-specified backward origin |

double |

getConstant()

Returns the constant parameter estimate. |

double[] |

getDeviations()

Returns the deviations used for calculating the forecast confidence limits. |

double[] |

getForecast(int nForecast)

Returns forecasts |

double |

getInnovationVariance()

Returns the variance of the random shock. |

double[] |

getMA()

Returns the final moving average parameter estimates. |

double |

getMean()

Returns an update of the mean of the time series z. |

int |

getNumberOfBackcasts()

Returns the number of backcasts used to calculate the AR coefficients for the time series z. |

double[][] |

getParamEstimatesCovariance()

Returns the covariances of parameter estimates. |

double[] |

getPsiWeights()

Returns the psi weights of the infinite order moving average form of the model. |

double[] |

getResidual()

Returns the residuals. |

double |

getSSResidual()

Returns the sum of squares of the random shock. |

double |

getVariance()

Returns the variance of the time series z. |

void |

setARLags(int[] arLags)

Sets the order of the autoregressive parameters. |

void |

setArmaInfo(double constant,

double[] ar,

double[] ma,

double var)

Sets the ARMA_Info Object to previously determined values |

void |

setBackcasting(int maxBackcast,

double tolerance)

Sets backcasting option. |

void |

setBackwardOrigin(int backwardOrigin)

Sets the maximum backward origin. |

void |

setCenter(boolean center)

Sets center option. |

void |

setConfidence(double confidence)

Sets the confidence level for calculating confidence limit deviations returned from getDeviations. |

void |

setConvergenceTolerance(double convergenceTolerance)

Sets the tolerance level used to determine convergence of the nonlinear least-squares algorithm. |

void |

setInitialEstimates(double[] ar,

double[] ma)

Sets preliminary estimates for the LEAST_SQUARES estimation

method. |

void |

setMALags(int[] maLags)

Sets the order of the moving average parameters. |

void |

setMaxIterations(int iterations)

Sets the maximum number of iterations. |

void |

setMean(double zMean)

Sets an initial estimate of the mean of the time series z. |

void |

setMethod(int method)

Sets the estimation method used for estimating the ARMA parameters. |

void |

setRelativeError(double relativeError)

Sets the stopping criterion for use in the nonlinear equation solver. |

| Methods inherited from class java.lang.Object |

|---|

clone, equals, finalize, getClass, hashCode, notify, notifyAll, toString, wait, wait, wait |

| Field Detail |

|---|

public static final int LEAST_SQUARES

public static final int METHOD_OF_MOMENTS

| Constructor Detail |

|---|

public ARMA(int p,

int q,

double[] z)

ARMA.

p - an int scalar containing the number of

autoregressive (AR) parametersq - an int scalar containing the number of moving

average (MA) parametersz - a double array containing the observations

IllegalArgumentException - is thrown if p,

q, and z.length are not

consistent.| Method Detail |

|---|

public final void compute()

throws ARMA.MatrixSingularException,

ARMA.TooManyCallsException,

ARMA.IncreaseErrRelException,

ARMA.NewInitialGuessException,

ARMA.IllConditionedException,

ARMA.TooManyITNException,

ARMA.TooManyFcnEvalException,

ARMA.TooManyJacobianEvalException

ARMA.MatrixSingularException - is thrown if the input matrix is

singular.

ARMA.TooManyCallsException - is thrown if the number of calls to

the function has exceeded the maximum number of iterations times the

number of moving average (MA) parameters + 1.

ARMA.IncreaseErrRelException - is thrown if the bound for the

relative error is too small.

ARMA.NewInitialGuessException - is thrown if the iteration has not

made good progress.

ARMA.IllConditionedException - is thrown if the problem is

ill-conditioned.

ARMA.TooManyITNException - is thrown if the maximum number of

iterations is exceeded.

ARMA.TooManyFcnEvalException - is thrown if the maximum number of

function evaluations is exceeded.

ARMA.TooManyJacobianEvalException - is thrown if the maximum number

of Jacobian evaluations is exceeded.public final double[][] forecast(int nForecast)

nForecast - an int scalar containing the maximum

lead time for forecasts. nForecast

must be greater than 0.

double matrix of dimensions of

nForecast by backwardOrigin + 1

containing the forecasts. The forecasts are for

lead times z.length-backwardOrigin-1+j where

NULL if the least-square estimates of parameters

is not computed.public double[] getAR()

compute method must be invoked first before invoking this

method. Otherwise, the method throws a NullPointerException

exception.

double array of length p containing

the final autoregressive parameter estimatespublic double[] getAutoCovariance()

z. Note

that the compute method must be invoked before this method.

Otherwise, the method throws a NullPointerException exception.

double array containing the autocovariances of

lag k, where k = 1, ..., p + q + 1public int getBackwardOrigin()

int scalar containing the user-specified

backward originpublic double getConstant()

compute method must be invoked first before invoking this

method. Otherwise, the return value is NaN.

double scalar containing the constant parameter

estimatepublic double[] getDeviations()

double array of length nForecast

containing the deviations for calculating forecast confidence

intervals. The confidence level is specified in

confidence. By default, confidence=

0.95.public double[] getForecast(int nForecast)

nForecast - An input int representing the number

of requested forecasts beyond the last value in the

series.

double array containing the

nForecast+backwardOrigin forecasts. The first

backwardOrigin forecasts are one-step ahead

forecasts for the last backwardOrigin values in the

series. The next nForecast values in the returned

series are forecasts for the next values

beyond the series.public double getInnovationVariance()

double scalar equal to the variance of

the random shock.public double[] getMA()

compute method must be invoked first before invoking this

method. Otherwise, the method throws a NullPointerException

exception.

double array of length q containing

the final moving average parameter estimatespublic double getMean()

z. Note

that the compute method must be invoked first before

invoking this method. Otherwise, the return value is 0.

double scalar containing an update of the mean of

the time series z. If the time series is not

centered about its mean, and least-squares algorithm is used,

zMean is not used in parameter estimation.public int getNumberOfBackcasts()

z. Note that the compute

method must be invoked first before invoking this method. Otherwise,

the return value is 0.

int scalar containing the number of backcasts

calculated, this value will be less than or equal to

the maximum number of backcasts set in the

setBackcasting method.public double[][] getParamEstimatesCovariance()

compute method must be invoked first before invoking this

method. Otherwise, the method throws a NullPointerException

exception.

double matrix of dimensions of np by

np, where np = p + q + 1 if

z is centered about zMean, and

np = p + q if z is not centered,

containing the covariances of parameter estimates. The ordering

of variables is zMean, ar, and

ma.public double[] getPsiWeights()

forecast method must be invoked

first before invoking this method. Otherwise, the method throws a

NullPointerException exception.

double array of length nForecast

containing the psi weights of the infinite order moving average

form of the model.public double[] getResidual()

compute method must

be invoked first before invoking this method. Otherwise, the method

throws a NullPointerException exception.

double array of length z.length -

Math.max(arLags[i]) + length containing the residuals

(including backcasts) at the final parameter estimate point in

the first z.length - Math.max(arLags[i]) + nb,

where nb is the number of values backcast,

nb=ARMA.getNumberOfBackcasts(). This method is only applicable

using least-squares algorithm.public double getSSResidual()

compute method must be invoked first before invoking this

method. Otherwise, the return value is 0.

double scalar containing the sum of squares of

the random shock, residual is the array return from the

getResidual method and na = residual.length

. This method is only applicable using least-squares

algorithm.public double getVariance()

z. Note that the

compute method must be invoked first before invoking this

method. Otherwise, the return value is NaN.

double scalar containing the variance of the time

series zpublic void setARLags(int[] arLags)

arLags - an int array of length p

containing the order of the autoregressive parameters.

The elements of arLags must be greater than

or equal to 1. Default: arLags = [1, 2, ...,

p]

public void setArmaInfo(double constant,

double[] ar,

double[] ma,

double var)

constant - a double scalar equal to the constant

term in the ARMA model.ar - a double array of length p

containing estimates of the autoregressive parameters.ma - a double array of length q

containing estimates of the moving average parameters.var - a double scalar equal to the innovation

variance

public void setBackcasting(int maxBackcast,

double tolerance)

maxBackcast - an int scalar containing the maximum length

of backcasting and must be greater than or equal to 0.

Default: maxBackcast = 10.tolerance - a double scalar containing the

tolerance level used to determine convergence of the

backcast algorithm. Typically, tolerance

is set to a fraction of an estimate of the

standard deviation of the time series. Default:

tolerance = 0.01 * standard deviation

of z.public void setBackwardOrigin(int backwardOrigin)

backwardOrigin - an int scalar specifying the

maximum backward origin. backwardOrigin

must be greater than or equal to 0 and

less than or equal to z.length -

Math.max(maxar, maxma), where maxar = Math.max(arLags[i]), maxma =

Math.max(maLags[j]), and forecasts at

origins z.length - backwardOrigin

through z.length are generated.

Default: backwardOrigin = 0.public void setCenter(boolean center)

center - a boolean scalar. If false is

specified, the time series is not centered about its

mean, zMean. If true is

specified, the time series is centered about its mean.

Default: center = true.public void setConfidence(double confidence)

getDeviations.

confidence - a double scalar specifying the

confidence level used in computing forecast

confidence intervals. Typical choices for

confidence are 0.90, 0.95, and 0.99.

confidence must be greater than 0.0

and less than 1.0. Default: confidence = 0.95.public void setConvergenceTolerance(double convergenceTolerance)

convergenceTolerance - a double scalar containing

the tolerance level used to determine convergence of the

nonlinear least-squares algorithm.

convergenceTolerance represents the minimum

relative decrease in sum of squares between two iterations

required to determine convergence. Hence,

convergenceTolerance must be greater than or

equal to 0. The default value is eps = 2.2204460492503131e-16.

public void setInitialEstimates(double[] ar,

double[] ma)

LEAST_SQUARES estimation

method. The values of the autoregressive and moving

average parameters submitted are used as intial values for least squares

estimation. Otherwise they are initialized to values computed using the

method of moments. When the estimation method is set to

METHOD_OF_MOMENTS these initial values are not used.

ar - a double array of length p

containing preliminary estimates of the autoregressive

parameters. ar is computed internally if this

method is not used. This method is only applicable using

least-squares algorithm.ma - a double array of length q

containing preliminary estimates of the moving average

parameters. ma is computed internally if this

method is not used. This method is only applicable using

least-squares algorithm.public void setMALags(int[] maLags)

maLags - an int array of length q

containing the order of the moving average parameters.

The elements of maLags must be greater than or

equal to 1. Default: maLags = [1, 2, ...,

q]public void setMaxIterations(int iterations)

iterations - an int scalar specifying the maximum

number of iterations allowed in the nonlinear

equation solver used in both the method of moments

and least-squares algorithms. Default:

interations = 200.public void setMean(double zMean)

z.

zMean - a double scalar containing an initial

estimate of the mean of the time series z.

If the time series is not centered about its mean, and

least-squares algorithm is used, zMean is

not used in parameter estimation.public void setMethod(int method)

method - an int scalar specifying the method to be

use. If ARMA.METHOD_OF_MOMENTS is

specified, the autoregressive and moving average

parameters are estimated by a method of moments

procedure. If ARMA.LEAST_SQUARES is

specified, the autoregressive and moving average

parameters are estimated by a least-squares procedure.

Default method = ARMA.METHOD_OF_MOMENTS.public void setRelativeError(double relativeError)

relativeError - a double scalar containing the

stopping criterion for use in the nonlinear

equation solver used in both the method of

moments and least-squares algorithms. Default:

relativeError = 2.2204460492503131e-14.

|

JMSLTM Numerical Library 6.0 | |||||||

| PREV CLASS NEXT CLASS | FRAMES NO FRAMES | |||||||

| SUMMARY: NESTED | FIELD | CONSTR | METHOD | DETAIL: FIELD | CONSTR | METHOD | |||||||