com.imsl.stat.MultiCrossCorrelation

com.imsl.stat.MultiCrossCorrelation

|

JMSLTM Numerical Library 6.1 | |||||||

| PREV CLASS NEXT CLASS | FRAMES NO FRAMES | |||||||

| SUMMARY: NESTED | FIELD | CONSTR | METHOD | DETAIL: FIELD | CONSTR | METHOD | |||||||

java.lang.Object

public class MultiCrossCorrelation

Computes the multichannel cross-correlation function of two mutually stationary multichannel time series.

MultiCrossCorrelation estimates the multichannel cross-correlation

function of two mutually stationary multichannel time series. Define

the multichannel time series X by

![]()

![]()

x.length

and p = x[0].length. Similarly, define the multichannel time

series Y by

![]()

![]()

y.length and q = y[0].length.

The columns of X and Y correspond to individual channels

of multichannel time series and may be examined from a univariate

perspective. The rows of X and Y correspond to

observations of p-variate and q-variate time series,

respectively, and may be examined from a multivariate perspective.

Note that an alternative characterization of a multivariate time series

X considers the columns to be observations of the multivariate

time series while the rows contain univariate time series. For example,

see Priestley (1981, page 692) and Fuller (1976, page 14).

Let ![]() =

= xmean be the row

vector containing the means of the channels of X. In particular,

![]()

ymean be similarly

defined. The cross-covariance of lag k between channel i

of X and channel j of Y is estimated by

maximum_lag. The summation on t extends over all

possible cross-products with N equal to the number of

cross-products in the sum.

Let ![]() =

= xvar,

where xvar is the variance of X, be the row

vector consisting of estimated variances of the channels of X.

In particular,

![]()

![]()

yvar,

where yvar is the variance of Y, be similarly

defined. The cross-correlation of lag k between channel i

of X and channel j of Y is estimated by

![]()

| Nested Class Summary | |

|---|---|

static class |

MultiCrossCorrelation.NonPosVariancesException

The problem is ill-conditioned. |

| Constructor Summary | |

|---|---|

MultiCrossCorrelation(double[][] x,

double[][] y,

int maximum_lag)

Constructor to compute the multichannel cross-correlation function of two mutually stationary multichannel time series. |

|

| Method Summary | |

|---|---|

double[][][] |

getCrossCorrelation()

Returns the cross-correlations between the channels of x

and y. |

double[][][] |

getCrossCovariance()

Returns the cross-covariances between the channels of x

and y. |

double[] |

getMeanX()

Returns the mean of each channel of x. |

double[] |

getMeanY()

Returns the mean of each channel of y. |

double[] |

getVarianceX()

Returns the variances of the channels of x. |

double[] |

getVarianceY()

Returns the variances of the channels of y. |

void |

setMeanX(double[] mean)

Estimate of the mean of each channel of x. |

void |

setMeanY(double[] mean)

Estimate of the mean of each channel of y. |

| Methods inherited from class java.lang.Object |

|---|

clone, equals, finalize, getClass, hashCode, notify, notifyAll, toString, wait, wait, wait |

| Constructor Detail |

|---|

public MultiCrossCorrelation(double[][] x,

double[][] y,

int maximum_lag)

x - A two-dimensional double

array containing the first multichannel stationary

time series. Each row of x corresponds

to an observation of a multivariate time series and

each column of x corresponds to a

univariate time series.y - A two-dimensional double

array containing the second multichannel stationary

time series. Each row of y corresponds to

an observation of a multivariate time series and each

column of y corresponds to a univariate

time series.maximum_lag - An int containing

the maximum lag of the cross-covariance and

cross-correlations to be computed.

maximum_lag must be greater

than or equal to 1 and less than the

minimum number of observations of x and

y.| Method Detail |

|---|

public double[][][] getCrossCorrelation()

throws MultiCrossCorrelation.NonPosVariancesException

x

and y.

double array of size 2 *

maximum_lag +1 by x[0].length by

y[0].length containing the cross-correlations between

the time series x and y.

The cross-correlation between channel i of the x

series and channel j of the y series at lag

k, where k = -maximum_lag, ..., 0, 1, ...,

maximum_lag, corresponds to output array element with index [k][i][j] where

k= 0,1,...,(2*maximum_lag),

i = 1, ..., x[0].length,

and j = 1, ..., y[0].length.

MultiCrossCorrelation.NonPosVariancesException

public double[][][] getCrossCovariance()

throws MultiCrossCorrelation.NonPosVariancesException

x

and y.

double array of size 2 *

maximum_lag +1 by x[0].length by

y[0].length containing the cross-covariances between

the time series x and y.

The cross-covariances between channel i of the x

series and channel j of the y series at lag

k where k = -maximum_lag, ..., 0, 1, ...,

maximum_lag, corresponds to output array element with index [k][i][j] where

k= 0,1,...,(2*maximum_lag),

i = 1, ..., x[0].length,

and j = 1, ..., y[0].length.

MultiCrossCorrelation.NonPosVariancesExceptionpublic double[] getMeanX()

x.

double containing the mean

of each channel in the time series x.public double[] getMeanY()

y.

double containing the

estimate mean of each channel in the time series y.

public double[] getVarianceX()

throws MultiCrossCorrelation.NonPosVariancesException

x.

double containing the variances

of each channel in the time series x.

MultiCrossCorrelation.NonPosVariancesException

public double[] getVarianceY()

throws MultiCrossCorrelation.NonPosVariancesException

y.

double containing the variances

of each channel in the time series y.

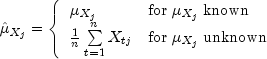

MultiCrossCorrelation.NonPosVariancesExceptionpublic void setMeanX(double[] mean)

x.

mean - A one-dimensional double containing the

estimate of the mean of each channel in time series

x.public void setMeanY(double[] mean)

y.

mean - A one-dimensional double containing the

estimate of the mean of each channel in the time series

y.

|

JMSLTM Numerical Library 6.1 | |||||||

| PREV CLASS NEXT CLASS | FRAMES NO FRAMES | |||||||

| SUMMARY: NESTED | FIELD | CONSTR | METHOD | DETAIL: FIELD | CONSTR | METHOD | |||||||