| StepwiseRegressionIntercept Property |

Returns the intercept.

Namespace: Imsl.Stat

Assembly: ImslCS (in ImslCS.dll) Version: 6.5.2.0

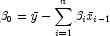

The intercept is computed as follows:

where

where  is the mean of the dependent

variable y,

is the mean of the dependent

variable y,  are the

coefficients, and

are the

coefficients, and  are the mean

values for each independent variable

are the mean

values for each independent variable  in

the final model. If the covariance matrix is used for input, use

method SetMean to specify the means of the variables. If

x and y are used for input, the means are computed

internally and do not need to be specified.

in

the final model. If the covariance matrix is used for input, use

method SetMean to specify the means of the variables. If

x and y are used for input, the means are computed

internally and do not need to be specified.